For those of us who enjoyed those Super Bowl wins of the 1990's in Dallas, we all know that the Dallas Cowboys became a franchise team under Coach Jimmy Johnson. Jerry had the money and the smarts to hire his old Arkansas Razorback teammate, but Coach Johnson brought the formula for success. It was honed in Florida at the University of Miami, where each Hurricane was conditioned to be faster, stronger, and have greater endurance than his competitor. As Coach Johnson explains in this video from ESPN's 30 for 30, "Fatigue makes cowards of us all."

Read MoreGetting "Fed Up" / Trends Not Sweet

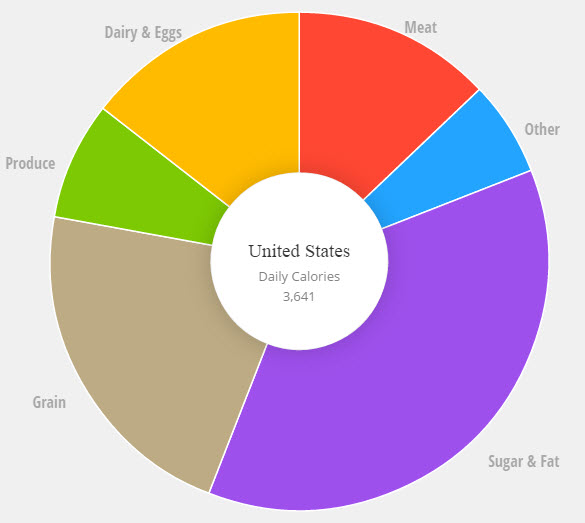

Almost 60% of the U.S. diet is made up of sugar and carbohydrate. Since 1977, Americans have doubled their daily intake of sugar, lurking in processed foods like cereal and catsup. Our sugar intake has lead to a corresponding rise in obesity, metabolic syndrome and chronic conditions that are the result of a pancreas that eventually exhausts itself from producing the hormone insulin.

Almost 60% of the U.S. diet is made up of sugar and carbohydrate. Since 1977, Americans have doubled their daily intake of sugar, lurking in processed foods like cereal and catsup. Our sugar intake has lead to a corresponding rise in obesity, metabolic syndrome and chronic conditions that are the result of a pancreas that eventually exhausts itself from producing the hormone insulin.

How could it be that from 1980 to 2000, fitness memberships doubled along with a corresponding doubling of the obesity rate? If our willpower is to blame why do we have obesity in 6 year olds? And of all the nutrients listed on a food label, how is it that sugar, a substance more addictive than cocaine, is the only nutrient that a food manufacturer does not have to disclose under the food label's percentage daily recommended allowance guidelines? Could it be that Americans were misled into believing that a "low-fat" diet was best for us based on junk science? Could federal guidelines have been influenced by powerful food lobbies and corporate profits placed ahead of our public health interests?

Realizing we now have an epidemic that we are not going to be able to exercise our way out of, the U.S. Preventive Task Force (USPTF) has recommended coverage for progams that have demonstrated clinical success in reversing symptoms of Metabolic Syndrome be covered under the Affordable Care Act (ACA) at 100% with no cost sharing. In a future post, I'll share more about how and when employers must cover behavioral weight management as a benefit and what our ACAP Health subsidiary is doing to help companies reverse these metabolic trends caused by sugar.

Our company will continue to endorse only programs that adhere to evidence based guidelines from trusted voices like Dr. David Katz, Dr. Mark Hyman, Dr. Robert Lustig, Tim Church, M.D., M.P.H., Ph.D and Dr. David Kessler. Please commit to watching "Fed Up", produced by Katie Couric and Laurie David.

Accountable Care - Transforming Healthcare Delivery

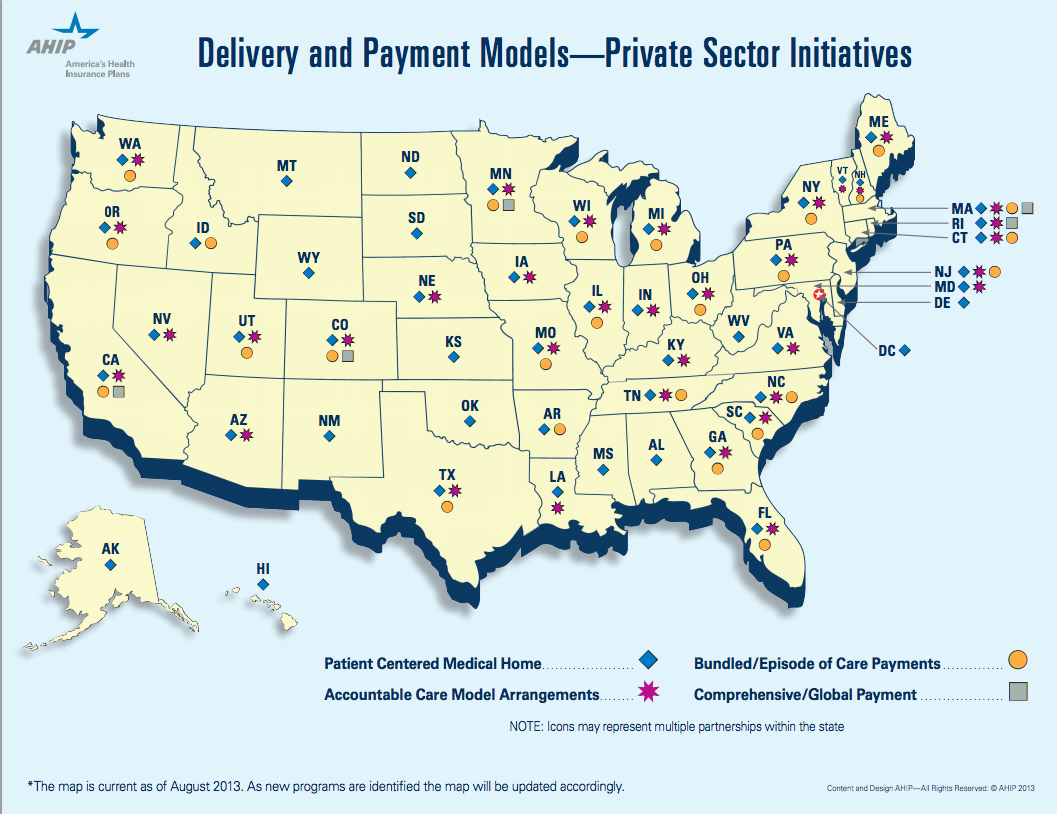

At no other time in the history of our country has the healthcare delivery system so rapidly transformed as it has since the passage of the Affordable Care Act (ACA). With healthcare consuming nearly 20% of our country's GDP, traditional fee for service medicine simply was not sustainable. Accountable Care Organizations ("ACO's") hope to change that with the aim of improving population health, improving the care experience and reducing the per-capita cost. The Centers for Medicare and Medicaid Services (CMS) have very clear rules and definitions as to what might comprise an ACO for the Medicare market, but when it comes to what it means for the private sector, definitions vary. An ACO is a health care delivery system that has partnered with a payer or purchaser of health care to develop arrangements that align financial interests with the delivery of effective and quality care for a specific population. However, if you have seen one ACO ... you have seen one ACO since success is contingent upon IT integration, physician-led affiliation, care coordination, access, prevention and convenience, and payment reform that aligns stakeholder interests.

Many plan sponsors might first think an ACO of today is simply warmed over "HMO soup", reheated from the 1990's. What's different is that we have advances in technology, larger systems of care with greater physician/hospital collaboration, bigger federal incentives and a decade of best practices to guide us. Many systems will be smart to avoid the mistakes made during the HMO era when the market greatly underpriced premiums, withheld care and failed to model risk accurately. We're only in the first inning of the ACO era that will continue to lead to pay for performance, bundled payments, episodic risk sharing and more fully capitated transfer of risk for health sytems.

According to Leavitt Partners latest study, there are over 600 ACOs now across the United States:

There are three considerations that should prompt employers of all sizes to consider ACO's in their employee benefits portfolio:

1) Available Now - Traditional health insurers, physician groups and health systems have been hard at work building partnerships that incorporate shared risk arrangements. Last year, ACOs began rolling their products out to our benefit consulting teams for us to share with our clients. We were pleased to learn the health systems and carriers are "eating at their own restaurant" by enrolling their employees into their own ACO over the last couple of years. For the early adopter seeking alternatives that promise greater value with a narrower network or steerage mechanisms, ACO options are available now throughout the country. Our firm has examples of clients who have deployed narrow network strategies in partnership with hospital based systems anchored in DFW. One of the largests now boasts a network of approximately 50 hospitals, 500 patient access points and 6,000 affiliated physicians.

2) Geographic Density - Since ACOs are about the delivery of healthcare at the local level, employers with great density (concentrations of a large number of employees) will fare better with this strategy. In California for instance, CALPERS, one of the state's largest plan sponsors, had enough clout to form a direct contract with a upside premium credit of nearly $16MM with a physicians group, Blues plan and hospital system. This alliance was formed to compete against the dominate player in the area, Kaiser of California. If you are the major employer in an area, you and other employers have more clout than you might think in this new era of ACO alignment.

3) Show Me the Money - The most fundamental change that ACOs may bring to the market is a substantial increase in the levels of collaboration among payors and providers. So how will more integrated models prove to the private sector they can truly remove waste, impact steerage, align incentives with greater patient satisfaction? These integrated systems realize they must offer up savings in the form of guarantees, ,risk-adjusted PMPMs and total cost guarantees for us to consider their offering. Initial actuarial projections are targeting PMPM savings ranging from 5-10% off of current spending levels, as contracts mature.

But accountability is up to every organization and every body with a body. The ACO cannot foster health alone ... and that's why the early adopters must be prepared to lead with executive sponsorship, design and contribution alignment to drive steerage, coordination and communications that lend support to these exciting options. I am a voracious reader of Benefits Quarterly, a publication for peers in my industry. This excerpt, written by Isabelle Wang and Michael Maniccia of Deloitte, provides a good primer for employers to consider on the topic of ACOs and is available on their website or download here:

Being Thankful - A Christmas to Remember

I landed in the middle of central Mexico and I had a 103 degree fever. It was our family trip scheduled over the Christmas holiday. We would celebrate my in-laws, Earl and Eileen Eliason's, 50th wedding anniversary. We were to arrive at Hacienda las Trancas in the state of Guanajuato, Mexico. As I stood in line waiting to show our visas to the customs officials, beads of sweat were forming on my brow. My eyes darted about reading posters about Ebola and the symptoms that would preclude a tourist from entering the country. It began to dawn on me that I might not make it into the country with my family. I made it through and was thrilled to find our welcoming party did not include trumpets, tequila, mariachis and sombreros. Wait ... that was Cancun 1990 with my college friends. Thankfully, our driver spoke little English and allowed me to sleep for 90 minutes in the front seat as we bumped along the Mexican highways to the small town of Trancas, Mexico. In the same way I conduct my business travel with little more than an iPhone and the map app, I had done little research on our destination. Over the course of the trip, I began to realize that just like America fought to declare its independence from British rule, Mexico was rich in revolutionary history in their triumph over Spain. This central part of Mexico was the epicenter where it all took place in the early 1800s. In other words, we were in the Boston, Massachusetts of Mexico. It would be a trip our family would always remember, as we pulled up to a 450 year old ex-hacienda. We felt like Spanish royalty entering a fortress through the giant wooden arched doors. My wife was smart to point me to an area we later called the infirmary. It was my own suite with a king-size bed where I slept for hours until my fever broke.

When I walked out into a daze into the courtyard, I realized that we were in the most magical of places in Central Mexico, north of San Miguel de Allende, Dolores Hidalgo and Guanajuato. The same site was photographed by Vogue magazine in this shoot. The dinner bell rang out at 6:00 p.m. I found the rest of the family (who somehow escaped my germs) at the dinner table waiting to be served. What's this ... a staff of fifteen would be caring for our every need and serving us homemade Mexican cooking (every fruit and vegetable was safe to eat). Each day also brought homemade tortilla chips and margaritas at 5:00 p.m. in the courtyard. At dinner, I made sure to keep my distance as we sat at a Spanish style table that was no less than 30 yards long. We were greeted by Yolanda, the sweetest Spanish cook and caretaker you could ever meet.

While our trips into each town provided cultural and artistic surprises, it was our sanctuary at the Hacienda that we looked forward to the most. Our two boys had a blast riding horseback and playing ping pong every day while Kristen and I enjoyed hot stone massages, riding bikes, reading books in the hammocks, watching the sunrise and sunset, and playing games with our family. There was even a full-service gym next to the spa that was as nice as most fitness centers in Dallas.

This Christmas was not full of the tradition of driving to different houses to open presents like we have done in years past. In fact, there were no presents to be opened at all with one exception ... Kristen and Lois had reached out to all of Earl and Eileen's friends and family over 50 years of marriage and asked if they would provide a memory, write a letter or furnish a picture for the anniversary book that was being secretly put together for Earl and Eileen. Watching them open the gift, cry together like two teenage sweethearts and savor every page was unforgettable. While all the credit goes to our awesome wives, it allowed us all to play a part in presenting a special gift to the two most deserving of recipients.

As our trip started coming to an end, we got concerned we were running out of time. Earl and Eileen concluded the celebration anniversary dinner by sharing some memories and Earl read a poem he wrote entitled a "Half Century Day". One of my favorite evenings was when the parents and kids all joined together to play Uno. As we pulled away from Hacienda las Trancas, we signed the guest book with the same wonderment we shared when we arrived. A half century day ... turned into a magical week ... full of cool nights and seventy degree days that our family will never forget. Memories made that will last a lifetime ... and 50 years of marriage celebrated in the grandest of style.

[smart-image-gallery]{"images":[{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Guanajuato-Mexico.jpg","title":"Guanajuato, Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2634"},{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Hacienda-Las-Trancas-2-Mexico.jpg","title":"Hacienda Las Trancas #2, Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2635"},{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Hacienda-Las-Trancas-Mexico.jpg","title":"Hacienda Las Trancas, Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2636"},{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Our-Room-1-Mexico.jpg","title":"Our Room #1 Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2637"},{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Our-Room-2-Mexico.jpg","title":"Our Room #2 Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2638"},{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Our-Room-3-Mexico.jpg","title":"Our Room #3 Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2639"},{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Purple-Flowers-Mexico.jpg","title":"Purple Flowers - Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2640"},{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Steve-with-Boys-in-Guanajuato-Mexico.jpg","title":"Steve with Boys in Guanajuato, Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2641"},{"url":"http://www.benefitu.net/wp-content/uploads/2014/12/Sunset-at-Hacienda-Mexico.jpg","title":"Sunset at Hacienda, Mexico","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2642"},{"url":"http://www.benefitu.net/wp-content/uploads/2015/01/IMG_0049_3.jpg","title":"Mexico - Celebrating Earl and Eileen's 50 years of marriage","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2660"},{"url":"http://www.benefitu.net/wp-content/uploads/2015/01/IMG_0085_2.jpg","title":"Mexico - Horse running in stables","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2661"},{"url":"http://www.benefitu.net/wp-content/uploads/2015/01/IMG_0044_2.jpg","title":"Mexico - Drew Harris and the \"Smiling\" horse","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2662"},{"url":"http://www.benefitu.net/wp-content/uploads/2015/01/IMG_0898_2.jpg","title":"Mexico - 50 years of memories - The Anniversary Book","author":"Steve Harris, CEBS","origin":"http://www.benefitu.net/?attachment_id=2663"}],"settings":{"gallery":"gallery_classic","autoplay":false,"caption":true,"author":false,"thumbnails":false,"vertical":false}}[/smart-image-gallery]

Just a Reminder

I have a friend, Kathy Duran-Thal, who is a dietician in Dallas. She loves to say that, “Your feet cannot outrun your mouth.”

Read MoreOil Change or Health Screening - Which do we value more?

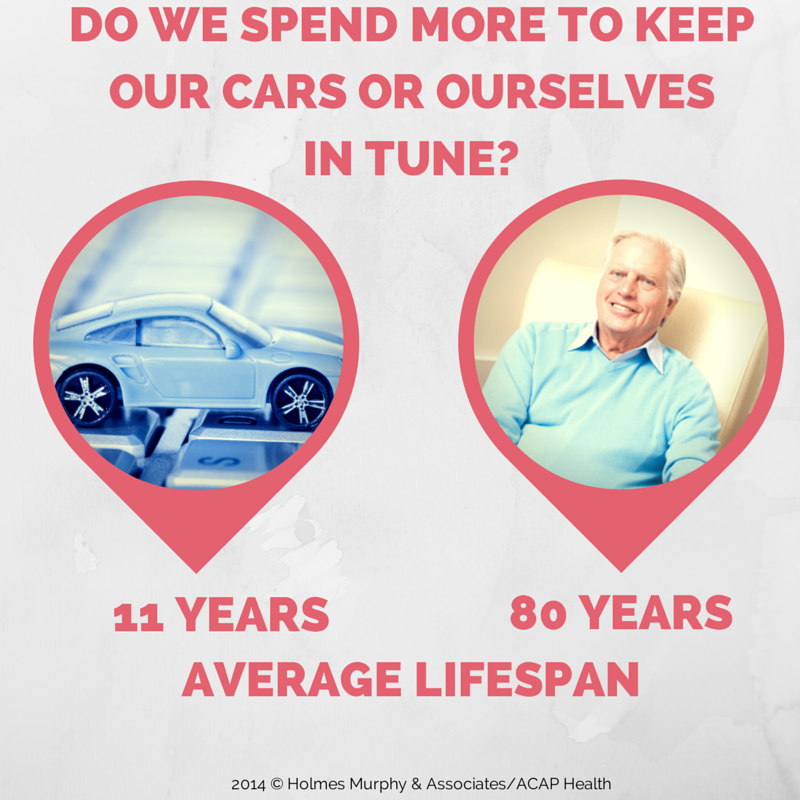

Americans have had a love affair with the automobiles ever since Henry Ford introduced the Model-T in 1908 to the Model S of today. With all the hype around new model releases, A USA Today article found that Americans are actually holding onto our existing cars for longer periods of time. The average lifespan of a car on the road increased from 8 to 11 years over the last two decades. There were two primary reasons cited why we drive our vehicles longer: advancements in technology and changes in the economy are forcing us to become more thoughtful consumers. Michael Calkins, AAA's manager of technical services, cited that this trend brings "a corresponding rise in maintenance and repair costs as our vehicles age".

These same economic forces are occurring in healthcare as one out of every eight Americans will be 65 or older by 2030. The average American now has a life span approximating 80 years old. So how much exactly should we be investing in ourselves each year to keep humming down life's highway? We were curious to learn if we spend a greater percentage of money to keep our cars or ourselves in tune.

We decided to look at how much we spend each year to keep the asset in good working order and compare it to the annual ownership cost for each asset. Consumer Reports gave us the average amount Americans spend to maintain their cars each year divided by the annual cost of ownership. The annual ownership cost of our health is a function of the premium we pay to insure ourselves. We calculated the average wellness spend at $728 per year divided by the total health costs an active employee costs to insure in the workplace at $11,830 per year.

We decided to look at how much we spend each year to keep the asset in good working order and compare it to the annual ownership cost for each asset. Consumer Reports gave us the average amount Americans spend to maintain their cars each year divided by the annual cost of ownership. The annual ownership cost of our health is a function of the premium we pay to insure ourselves. We calculated the average wellness spend at $728 per year divided by the total health costs an active employee costs to insure in the workplace at $11,830 per year.

Surprisingly, our findings showed we spend the same percentage on both. Six cents of every dollar was spent to keep both of these assets in working order each year. Investing the same percentage in each might make sense if each asset depreciated at the same rate. The reality of this finding is that the less important asset we drive for eleven years and the more important asset (for most Americans) is driven into the ground for eighty.

At ACAP Health, our business models forecast plan sponsors will do better by investing closer to 10% of health spend towards prevention, as compared to the industry average of 6%. The right allocation will vary based on the demographics of your workforce, with additional screenings and diagnostic costs correlating with age. As technology enables more sophisticated modeling, we'll continue to see investments made in what I'm calling the "Preventive Economy". This approach to risk management will impact policy decisions on everything from climate change to obesity. And it will force health payors to reevaluate their current prevention vs. sickness allocation of health spend. Our company's big data analytics warehouse now incorporates 47 million lives and case studies using clinical algorithms tied to one's metabolic risk factors to help us better illustrate the trade-offs between a "pay a little now versus a lot later" approach to health plan sponsorship.

The Preventive Economy will also change the way these services are delivered. Think of the full-service gas and repair stations as the doctor's offices of today compared to the Jiffy Lube's in healthcare emerging for tomorrow. Accountable care, patient centered medical homes, retail pharmacy, telehealth and consumer directed models of preventive maintenance and diagnostic care are coming to the rescue to shore up the scarcity of primary care and nurse practitioners. The preventive economy foreshadows these services will be in strong demand to address the scarcity of supply needed for the coming age boom.

So as you evaluate next year's healthcare spend make sure you are investing more than low single digits towards preventive maintenance to avoid your engine light coming on ... because establishing a healthy lifestyle of keystone habits is the closest thing you'll find to an 80 year bumper to bumper warranty.

CHICKEN LITTLE WAS RIGHT!

When it comes to the health of our country, Chicken Little was right…the sky IS falling!

Read More"We Are What We Do" by Tim Church, M.D., M.P.H., Ph.D.

Living well and living long are two different things. and one of the country's leading preventive health researchers, Dr. Tim Church, states it plain and simple—maintaining a high quality of life means finding time for physical activity.

Dr. Tim Church, Holmes Murphy & Associates / ACAP Health Medical Director on exercising your right to a better quality of life

One of the things I've really learned in medicine is that there are certain things that resonate with us that we believe in, with or without data – it just must be true. And the idea of, 'we are what we eat,' it is amazing to me how people hold onto that. People have a hard time getting their arms around, 'we are what we do.'

As a physician, through med school, through residency, I just got frustrated with treating things that were 100 percent preventable. And, you know, I love to say we like to heroically clean up after the car accident, but we don't like to put up stop signs. And, I just was always drawn towards prevention and then in my prevention quest so to speak, physical activity and exercise just made so much sense. It didn't matter what the analysis was. It didn't matter what we were looking at. There was always this one variable that was so powerful. It was exercise.

When it comes to weight loss one of my favorite sayings is: you diet to lose weight, and you exercise to keep it off. It doesn't matter what the macronutrient components of that diet are. You can focus on low carbs. You can focus on low protein. You can focus on low fat. It doesn't really matter. It tends to be an individual thing.

But, once you get the weight off, exercise becomes so critical in keeping it off. It's not hard to lose weight. It's very easy to lose weight, that's why all the fad diets work. That's why all this bogus stuff works. The challenge is keeping the weight off, keeping it off at six months, keeping it off at 12 months, keeping it off at two years.

Everything counts. If you're doing nothing now, this is not all or nothing, this is not about, 'hey if you don't get to 150 minutes a week, then it's a waste of time.' Just getting off the couch has benefits. In fact, the most sedentary individuals who have the worst health are the ones that benefit the most from a little bit of physical activity. The return on investment for a little bit of physical activity is huge for those guys. The person who's running a 10K all the time and ramps it up to a marathon. They don't get any more benefit when they go from 10K to marathon, they've already kind of maxed out. But that person who's totally sedentary and takes up a walking program? Huge benefits.

It's not about how long you're gonna live. How long you're gonna live is primarily determined by how long your grandparents lived, how long your parents lived. It's about how long you live well. Can you go duck hunting in your 80s? Can you chase your grandkids? You know, can you do the things that you love doing? And there's no pill for that. We can't go to the doctor and get a pill for quality of life. There's one thing we know that works for maintaining quality of life. And that is being physically active. That is leading an active lifestyle which may or may not include formal exercise. So, you want to lead the life you want to lead? You've got to be physically active.

© 2014 ShareWIK Media Group, LLC. All Rights Reserved.

Benefits Insight from a Twitter Founder

Jack Dorsey, the founder of Twitter (and now Square) once famously quipped that as business leaders we should "make every detail perfect and limit the number of details to perfect".

As employee benefit advisers, human resource and benefit professionals and service providers deal with new regulations, burden shifting and changing roles in a fast-changing employee benefits industry, we sometimes lose sight of who we are serving. As long as an employer is paying the majority of the costs, the employee benefit programs is an investment that reflects the culture and value placed upon the people in the organization.

Jack Dorsey, the founder of Twitter (and now Square) once famously quipped that as business leaders we should "make every detail perfect and limit the number of details to perfect".

As employee benefit advisers, human resource and benefit professionals and service providers deal with new regulations, burden shifting and changing roles in a fast-changing employee benefits industry, we sometimes lose sight of who we are serving. As long as an employer is paying the majority of the costs, the employee benefit programs is an investment that reflects the culture and value placed upon the people in the organization.

It might surprise some business owners to learn that the "perceived" value of the benefits actually has less to do with the family out-of-pocket amount and office visit copay and more to do with benefit experiences throughout the year. This was reinforced through a study by Deloitte that identified the high direct and indirect expense of turnover when good people leave their jobs because of bad management and poor culture. Employee benefits did not even make the top ten list of the reasons to jump ship.

Sure, getting the benefits design of your programs to reflect your company's core beliefs is an important first step along with selecting the right service providers and making sure we are in federal and state compliance. But all too often we run out of time to pay attention to the details that matter most ... the enrollment and user experience for our customer. Selecting a plan provider and paying the majority of the premium is hardly where the responsibility ends.

Have you seen this before in your benefit materials ... Call this number to set up an appointment, fax this form to this group, set up another user name and password to qualify for this, watch this video and fill out this form to get this, do these 10 meaningless things that will not impact your health ... and my favorite ... read this ... but don't take any action now (I just want you to inform you of these things that will add more stress to your world ... along with work and family obligations, missing planes, Ebola viruses, impending Cold War and Middle East unrest) but check back later for more details from your HR team. Also, plan to keep an an eye out in your inbox for more important dribble about your employee benefits that does not have any call to action or benefit to you or your family members.

Jack Dorsey gets it right ... because he cares about the ultimate detail, design and user experience. Twitter was about a simpler way to communicate. Square and Apple Pay are trying to improve the buying experience. When it comes to delivering employee benefits, we are always on target if we ask how we can make the service experience better for those whom we serve.

No Health Insurance - IRS Shows Us How Penalty Is Calculated

If your like me ... you may have thought the IRS penalties imposed for not having health insurance under the new ACA federal healthcare rules simply utilized the greater of 1% or $95 calculation by applying 1% times adjusted gross income.

If your like me ... you may have thought the IRS penalties imposed for not having health insurance under the new ACA federal healthcare rules simply utilized the greater of 1% or $95 calculation by applying 1% times adjusted gross income.

This week, Ed Oleksiak, JD, Holmes Murphy's national compliance lead, walked our consulting teams through how the the IRS will apply the penalty. So the 1% individual penalty is not just 1% times your income. You actually subtract a base amount which is the minimum thresholds for being required to file a tax return determined by filing status and then the 1% is multiplied times the resulting net income amount. The starting amount is household income. We are including a definition and example below.

Household income is the adjusted gross income from your tax return plus any excludible foreign earned income and tax-exempt interest you receive during the taxable year. Household income also includes the incomes of all of your dependents who are required to file tax returns.

Example: Single individual with $40,000 income

Jim just plain does not like politics or federal mandates. He is an unmarried gun-toting, iPhone 5s carrying young invincible with no dependents. He pays service fees each month to access his Match.com account ... but feels paying monthly health insurance premiums does not help him with the ladies. Jim does not have minimum essential coverage for any month during 2014 and does not qualify for an exemption. For 2014, Jim's household income is $40,000 and his filing threshold is $10,150.

To determine his payment using the income formula, subtract $10,150 (filing threshold) from $40,000 (2014 household income). The result is $29,850. One percent of $29,850 equals $298.50.

Jim's flat dollar amount is $95.

Because $298.50 is greater than $95 (and is less than the national average premium for bronze level coverage for 2014), Jim's shared responsibility payment for 2014 is $298.50, or $24.87 for each month he is uninsured (1/12 of $298.50 equals $24.87).

Jim will make his shared responsibility payment for the months he was uninsured when he files his 2014 income tax return, which is due in April 2015.

2014 Federal Tax Filing Requirement Thresholds

|

Filing Status |

Age |

Must File a Return If Gross Income Exceeds |

|

Single |

Under 65 |

$10,150 |

|

65 or older |

$11,700 |

|

|

Head of Household |

Under 65 |

$13,050 |

|

65 or older |

$14,600 |

|

|

Married Filing Jointly |

Under 65 (both spouses) |

$20,300 |

|

65 or older (one spouse) |

$21,500 |

|

|

65 or older (both spouses) |

$22,700 |

|

|

Married Filing Separately |

Any age |

$3,950 |

|

Qualifying Widow(er) with Dependent Children |

Under 65 |

$16,350 |

|

65 or older |

$17,550 |

Health Plan Identifier (HPID) - A Must Do by November 5th, 2014

If your company sponsors a health plan (excluding small plans), and you have administrative oversight of that plan, you must get a Health Plan Identifier (HPID) under HIPAA by November 5th, 2014. You might be saying, I already have a lot on my plate or I would rather wait to do this in November. Sure, you could wait until things get slower around the fall during open enrollment or look into this before the holidays. Or you or a member of your HR/Benefits team could knock it out today.

Here are the instructions our firm put together to assist our clients.

This is being required by our federal government ... don't shoot the messenger ... we are simply trying to urge our clients to do this now.

Carrots and Sticks are for Donkeys and Mules

The following is a must watch for anyone who endeavors to change the health risk of a population. Our industry needs to move beyond treating our people like they are asses. We assume humans are like farm animals motivated by dangling a carrot or giving a smack on the rear. As Dr. BJ Fogg explains in the video below, an employee's level of motivation is hardly the culprit.

The research and understanding of "B=MAT" - behavior = motivation, ability and trigger ... is worth the small time investment it will take to watch this video. Dr. Fogg’s research is some of the most groundbreaking in terms of how human beings change behavior. Dr. B.J. Fogg is the Director of the Persuasive Technology Lab at Stanford University.

I came across this video at Rock Health when launching my own startup in the digital health technology space.

The HSA Turns Ten

There are some larger than life personas residing in Dallas who have had a profound impact on shaping our nation's health care system. It was December of 2003 when President Bush had just signed into law the Medicare Prescription Drug Improvement and Modernization Act. John Goodman, head of the Dallas based National Center for Policy Analysis (NCPA), helped give birth to provisions of the bill having contributed much of the thinking around HSA's and how a consumer's right to vote with their own pocketbook could change the health care marketplace.

While Goodman may have been the mother who conceived of the HSA and George W. Bush the father of the bill, this tax-advantaged baby got delivered to my team's front door step while consulting with a Fortune 500 client out of Austin, TX. It was 2003 and this company's leadership team was wrestling with an unsustainable health trend and a culture ready for change. They were the first and largest company in Texas to launch a qualified High Deductible Health Plan (HDHP) with an HSA in 2004. From conception of the design to the final delivery to employees, this work was significant and groundbreaking as employees at this company began to learn to use insurance for its intended purpose.

There are some larger than life personas residing in Dallas who have had a profound impact on shaping our nation's health care system. It was December of 2003 when President Bush had just signed into law the Medicare Prescription Drug Improvement and Modernization Act. John Goodman, head of the Dallas based National Center for Policy Analysis (NCPA), helped give birth to provisions of the bill having contributed much of the thinking around HSA's and how a consumer's right to vote with their own pocketbook could change the health care marketplace.

While Goodman may have been the mother who conceived of the HSA and George W. Bush the father of the bill, this tax-advantaged baby got delivered to my team's front door step while consulting with a Fortune 500 client out of Austin, TX. It was 2003 and this company's leadership team was wrestling with an unsustainable health trend and a culture ready for change. They were the first and largest company in Texas to launch a qualified High Deductible Health Plan (HDHP) with an HSA in 2004. From conception of the design to the final delivery to employees, this work was significant and groundbreaking as employees at this company began to learn to use insurance for its intended purpose.

According to the Employee Benefits Research Institute (EBRI), since the bill was signing into law, HSAs have since grown to 16.6 billion dollars in assets. In 2013, these assets grew 5.3 billion, a jaw dropping 47% increase over 2012 assets. Meanwhile, Health Reimbursement Arrangements (HRAs) are moving in the opposite direction with assets shrinking by 2% to 5.7 billion dollars last year.

There is a massive shift taking place in the market as consumer's continue to shoulder more of the out-of-pocket expense of health care and demand greater transparency over quality and cost. It has forced hospitals and physicians to cope with collections and bad debt since "we the people" are not always as reliable paying our bills as a large insurer. HSA linked plans have also sparked innovations from new swipe-card technology to alternative forms of free market care delivery.

While our country's legislators and many employers are currently fixated on purchasing health insurance, the real challenge over the next decade will be how incentives can be aligned to produce systemic behavior change that leads to the reduction and production of disease.

In 2013, more than 15 million individuals were enrolled in HSA-linked plans, a 50% increase in just three years. In 2014, reports indicate about 18% of employees will enroll in a tax-advantaged accounts linked to a high deductible plan. Here are a few reasons why HSA's will continue to thrive over the next decade:

1. Taxes are high - Marginal tax rates are at 39.6% and corporate taxes exceed those of other industrialized countries. Adopting tax-efficient plan design strategies like maximizing annual and catch-up contribution limits and using captives where appropriate will make sense for astute plan sponsors who care enough to reduce their own corporate and their employee's tax burden.

2. Qualified High Deductible Plans Are No Longer "High" - The minimum deductible and out-of-pocket requirements may have seemed high in 2003, but the 2014 minimum annual deductible of $1,250 is not that far from the $1,100 average annual deductible nationwide and well below the $1,700 average for small firms (under 200 workers). By the way, just because the legislators called it a "high" deductible health plan does not mean you need to promote it as such when you roll it out to your employees. Ask your benefits communication team to come up with something snappier.

3. They cost employers less - HSA linked plans cost employers about $1,700 less per employee compared with traditional PPO plans, according to a 2013 Mercer survey. In one of the first studies of its kind, EBRI found HSA linked plans reduced total health care spending by 25% in its first year and over the succeeding three years — albeit at a slower pace.

So Happy Birthday HSA ... It's time to toast you and those who nurtured you to ten. Here's to another a decade of market-driven progress enabling those who take measurable steps to improve their health to continue investing in themselves.

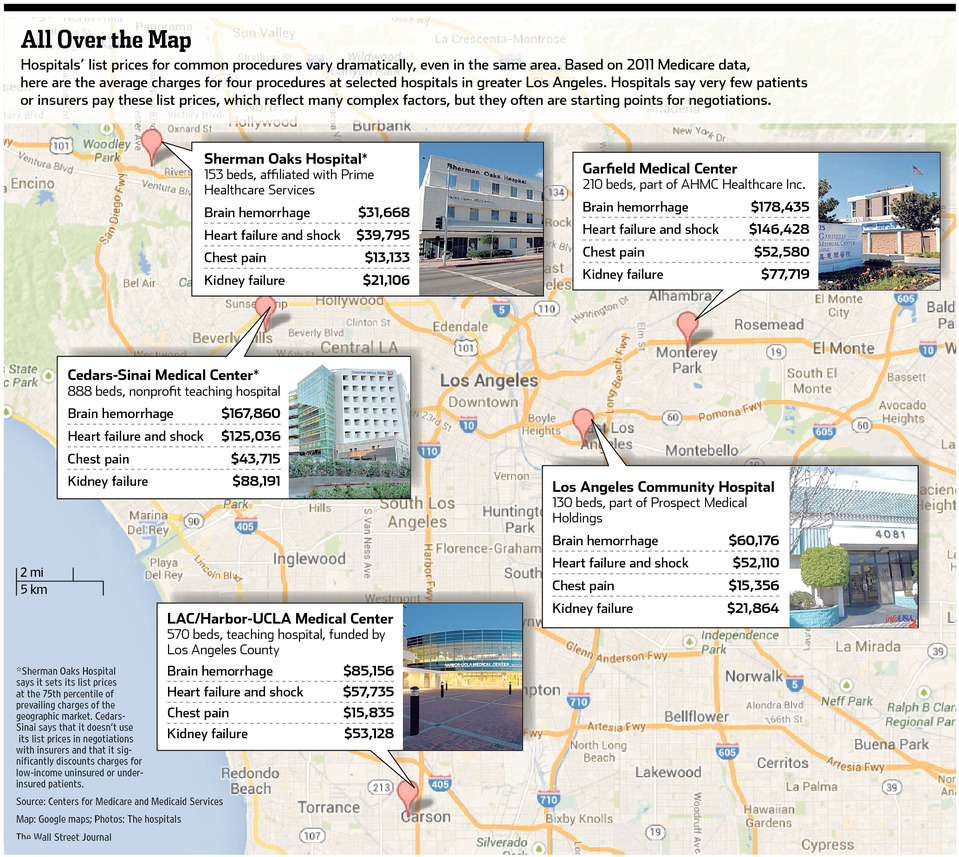

Health Care Pricing ... All Over the Map

It's always fun to watch shoppers each holiday season camp out for hours to snap up bargains that pale in comparison to the savings available in the health care marketplace. If buyers put as much emphasis on shopping for health services throughout the year as we do on enrolling for coverage once a year, we could make greater strides to flatten the cost trajectory of care.

If there is one city that knows how to shop it's Big D, so here's a three-step process for any employer hoping to put a little "Black Friday" in their health plan:

It's always fun to watch shoppers each holiday season camp out for hours to snap up bargains that pale in comparison to the savings available in the health care marketplace. If buyers put as much emphasis on shopping for health services throughout the year as we do on enrolling for coverage once a year, we could make greater strides to flatten the cost trajectory of care.

If there is one city that knows how to shop it's Big D, so here's a three-step process for any employer hoping to put a little "Black Friday" in their health plan:

1. Offer A High-Deductible Plan:

A 'quiet revolution in health insurance' is taking place as the number of employees enrolled in a plan with an annual deductible of $1,000 or more has risen to nearly 40% in 2013. Among all plans, the average annual deductible among covered workers is over $1,100 and exceeds $1,700 for small firms (under 200 workers). (Kaiser/HRET Survey of Employer Sponsored Health Plans).

Milton Friedman wisely quipped "Nobody spends somebody else's money as wisely as he spends his own. Putting in a high deductible plan enables your employees to be economically rewarded for shopping around and strategically aligns your insurance plan to cover infrequent and high cost medical events.

2. Arbitrage your Network

In the 20th century days of health care consulting, we used to attend to great detail to reprice claims for employers wanting to select the right insurer and network health plan. This focus on network discount has given way to more sophisticated value equation models. Once your health plan/network is in place, the employer must then teach employees to exploit hidden value within the network throughout the year.

60% of medical and pharmacy claims come from non-emergent services. As an example, three facilities within a five-mile radius in Dallas offer the same in-network MRI for prices ranging from $600 to $3,000. Transparency laws are now enabling big data analytics software to quickly review over a billion national claim records for price and quality comparisons at the push of a button.

3. Shop with a trusted friend

The best health price transparency providers have realized that shopping for care is best delivered when technology is married with an independent consumer advocate. As an example, there are over thirty types of knee surgery, so having a personal concierge to help me navigate my options enables my family to build trust with an advisor that does not have a financial interest in the outcome. To revolutionize the system, we need to help our employees act on information, not just provide data.

Many DFW employers are well on their way to creating a shoppers mentality among their health plan enrollees. Consumer advocacy and pricing transparency programs have already returned annualized savings anywhere from four to twenty-four times the cost of the service.

In a town that continues to reinvent the shopping experience, we anticipate more companies to get on the "Black Friday" bandwagon when it comes to savings in their health plan. The best part is we can all be empowered to score health deals that would make a Walmart clerk gush just by picking up the phone.

Top Ten Healthcare Predictions for 2014

1. With UT falling to Baylor, another 50/50 season for the Dallas Cowboys and a botched HealthCare.gov rollout in 2013, predictions for 2014 have head coach, Jason Garrett and U.S. Secretary of Health and Human Services, Kathleen Sebelius joining the ranks of Mack Brown and the unemployed ... At least they will have a new health insurance option available to them when they leave their employer.

2. Consumer health devices, mobile and telehealth initiatives will continue to bring about market-based reforms that enable better tracking, monitoring, and care coordination for patients with chronic conditions, who lack access to primary and specialty care or for those payers and providers willing to experiment with technology enabling solutions.

1. With UT falling to Baylor, another 50/50 season for the Dallas Cowboys and a botched HealthCare.gov rollout in 2013, predictions for 2014 have head coach, Jason Garrett and U.S. Secretary of Health and Human Services, Kathleen Sebelius joining the ranks of Mack Brown and the unemployed ... At least they will have a new health insurance option available to them when they leave their employer.

2. Consumer health devices, mobile and telehealth initiatives will continue to bring about market-based reforms that enable better tracking, monitoring, and care coordination for patients with chronic conditions, who lack access to primary and specialty care or for those payers and providers willing to experiment with technology enabling solutions.

3. Watch for continued M&A activity with health systems similar to Baylor Scott & White or Tenet (Vanguard Health) in other areas of the country. Health care delivery systems will continue to survive and thrive through specialization, mergers, or partnerships that lead to even bigger systems of care.

4. After the elections in November 2014, more carriers will exit the exchange system or become even more selective with their markets and propose double digit premium rate increases as the demographic underpinnings of the exchange fail to capture the 18-34 age group needed for the law to succeed.

5. With less than predicted young people signing up for HealthCare.gov, watch for legislative push to increase penalties for those who did not adhere to the requirements in the law in 2014. There will also be a healthy amount of debate over whether the penalties should be waived in 2014 due to the botched website rollout of healthcare.gov. [The penalty for 2014 is the greater of $95 a year or 1% of adjusted gross income].

6. The political rhetoric of "repeal and replace" will eventually give way to the demands of the American people searching for bipartisan amendments and solutions that target the real enemy in this country ... a broken fee for service environment that pays for the reimbursement of treating disease. The government will not shut down in 2014.

7. Employers will continue to adopt tax-efficient plans (such as high deductible health plans with health savings accounts) as new taxes (associated with ACA's funding) become more transparent to higher wage earners. Private health exchanges will grab the attention of employers interested in defined contribution approaches to funding their benefits.

8. Companies will abandon large incentives associated with traditional first generation wellness offerings (HRA's, Biometrics, and Wellness Content) in favor of programs that actually show promise of changing behavior to combat the effects of smoking, obesity, metabolic syndrome and diabetes — Pharmacotherapy and surgical options will gain more traction for those who qualify.

9. Watch for the continued proliferation of programs that provide price transparency and consumer advocacy. Consumers and large payers will become more educated around the disparity in pricing among health care facilities and providers. Congress will try and respond with everything from price controls to transparency bills.

10. Congress will not be able to agree to the Medicare cuts that are the underpinnings of the Affordable Care Act. The Office of Management and Budget (OMB) will run new actuarial calculations that increase the size of the federal deficit beyond what our children can bear.

The One Thing Needed for Exchanges to Succeed

Young people are the most coveted of all participants to have enrolled in a health insurance plan. It is the concept that underlies group underwriting to have those with fewer health risks to help offset the cost of those who are older and have greater medical needs. Dallas ranks as one of the largest communities of uninsureds in Texas at 31% compared to a 26% state average. Many of these uninsureds are young people (ages 18-35) who have relied on our public health system to be there if things do not go as planned.

The very success of the Affordable Care Act (ACA) will depend upon convincing these "young invincibles" that health protection is worth purchasing. If only the public exchanges could be as inviting as an Abercrombie & Fitch, Hollister or a Juicy Couture. The federal government is projecting enrollment in the exchange system to be around 7-8 million by the end of 2014. As the law intends, the cost of insuring the most expensive users of the system must be offset by around 2.7 million of young invincibles between the ages of 18-35 for it to work. In the first month of enrollment, 26,794 people selected a health plan on the federal exchange website. The makeup of these enrollees has not been released by the federal government, but a demographic match to the patronage of a cafeteria restaurant is to be expected.

As exchange enrollment begins to materialize in 2014, public officials may wish to revisit the following if they hope to enroll the most coveted young adults:

1. A Retail Experience That Works - When the standard young people are used to is designing their own Nike shoes online or ordering Uber's transportation service at the push of a button, HealthCare.gov will find itself quickly falling off the browser's "favorites" list. In a November survey by USA Today, many young people will not try again until December and cannot even comprehend calling a 1-800 number for service. We all like using intuitive technology that works ... but young people demand it even more ... a problem plaguing HealthCare.gov for the foreseeable future.

2. Changes to Employer Plan Dependent Definition - Many employer plans used to only cover dependent children up to age 19 or 26 (if a full-time student). On January 1, 2014, all employers (grandfathered and non-grandfathered) will be required to extend coverage to dependents up to age 26. The chief actuary at CMS is likely regretting the legislature's decision to extend dependent coverage to age 26 for employers. With 60% of American's covered by employer-based plans, this leaves a smaller group of of younger adults to enroll under the public exchanges.

3. Affordable Coverage - Older Americans will pay a higher rate than younger Americans, but the community rating is tiered using only three different age group bands. AARP lobbied strongly for this and it is an absolute boon to the baby boomers and a real shaft to Generation X, Y, and millennials who will bear the brunt of the top third-oldest risk tier by age. Age rating bands of 3:1 will prevent insurers from charging an adult age 64 more than three times the premium they charge a 21-year-old for the same coverage. As a result, young Americans will see higher premiums under the Exchanges than when they could have purchased coverage (Pre-ACA) in the private market when they used age rating bands of 5 to 1.

The Obama administration's federal study found that if all 50 states had expanded their Medicaid coverage the way they were supposed to when the law was passed, almost 90 percent of single Americans under 35 years could get coverage that cost less than $100 a month. They did not count on a Supreme Court ruling that enabled 25 states to opt out of expanding Medicaid coverage. This created unexpected "cracks" in the system when many young people who were to have qualified for Medicaid coverage will find they do not earn enough for subsidies under the Exchange.

In an astute political move, the Obama administration pushed back the requirements to release projected increases in health premiums for 2015 until after the November 2014 elections. In 2014 our young adults will eventually have to make a decision to pay the federal penalty (the greater of greater of $95 or 1% of AGI annually) or buy health coverage. Here's betting their XBox One they pay for neither.

Struck by Turtle? There's a Code for That

GOVERNMENT UPDATE: LIKE MOST REFORMS CONTROLLED BY A HEAVY HANDED BUREAUCRACY ... RULES WERE CHANGED MIDSTREAM PROMPTING OUR FREE MARKET SYSTEM TO REACT AGAIN TO UNEXPECTED CHANGES IN THE WAY HEALTH CARE IS REGULATED. THIS WAS THE RIGHT CALL TO DELAY THIS GIVEN BURDENS PLACED ON OUR CARE GIVERS . - APRIL 2014

The U.S. health care system will be implementing a new coding system called ICD-10 that is scheduled to take effect on October 1, 2014. The Centers for Medicare and Medicaid Services (CMS) will require the code sets be used by any covered entity under HIPAA (Health Insurance Portability Accountability Act). Whenever we are treated for medical care, a code is assigned to designate our illness or injury. These diagnosis codes are meant to help providers and payers better track what happened, how much it should cost and what follow-up care is needed.

The ICD-10 codes will not impact coding for outpatient procedures and physician services. There are around 13,000 codes under the current ICD-9 code set and an additional 55,000 coming next year. While the new 68,000 codes will yield enhanced reporting, the real beneficiaries in 2014 will be the IT providers who will charge more to implement the new CMS standards in their EMR systems. These costs will get passed along to payers and consumers in the form of higher prices for treatment.

Since our U.S. government is providing plenty of comedic fodder, it seemed like a good time to pile on and share some of our favorite codes:

- Struck by turtle, initial encounter: W5921XA

- Struck by turtle, subsequent encounter: W5922XD

- Hurt at the opera: Y92253

- Stabbed while crocheting: Y93D1

- Walked into a lamppost: W2202XA

- Walked into a lamppost, subsequent encounter: W2202XD

- Submersion due to falling or jumping from crushed water skis: V9037X

One of my favorite groups of codes relates to the rampant incidence of space-related injuries we often hear about. Thank goodness there are over ten codes for when a spacecraft goes out of control and plays a role in an injury. If you collided your spacecraft the first time use V9543XA. Do it once more and the hospital staff needs to use V9543XD for a subsequent encounter. How about codes for injuries with Macaws, Centipedes ... and others animals with from fur to feathers ... are available here.

Over 40 medical specialty groups, state organizations and the American Medical Association (AMA) have written letters to CMS recommending they cancel the implementation of ICD-10. The concern is that the new codes will "create significant burdens on the practice of medicine with no direct benefit to individual patient care." Additionally, the letters cite the burden of code implementations on top of a growing list of challenges doctors and hospitals have with the 2014 implementations of federal and state health care reforms.

So the next time you're injured from the dangers that lurk within the Winspear Opera House or you suffer a "burn due to flaming water-skis" ... just know that your federal government has you covered.

Photo Courtesy of PBS Newshour

Consumer Reports - Health Exchange Guidance

It seems ironic that we are on the eve of the October 1st, 2013 launch of the largest public open enrollment of health insurance in U.S. history and we are one day away from a government shutdown. While the rest of Washington D.C. tries to get its act together, we recognize that our friends in human resources may need a trusted resource to help navigate consumers through the impact of the Affordable Care Act (ACA). This year only, the health exchange marketplace open enrollment period will run from October 1, 2013, through March 31, 2014. In subsequent years, open enrollment will run from October 15th through December 7th, for a January 1st effective date. After this initial year only, the October 15th open enrollment schedule will match up with that of Medicare.

The older I get the more I rely on unbiased experts who can save me time and have my best interests at heart. This is why I am a subscriber to Consumer Reports. In the November 2013 issue, I was pleased to find a well constructed explanation of the ACA and how it might impact three different groups: someone who gets insurance through work, who buys insurance on their own, or who is Medicare eligible.

With over twenty years of benefits consulting experience, I thought I would put the Consumer Report's online guide called healthlawhelper.org to the test. I am giving it an enthusiastic thumbs up and hope you share it with those who come to you for help. It is a free resource that offers an easy to follow questionnaire that guides consumers through a personal decision making process on what to do. Consumer Reports is a national nonprofit organization with one and only one mission: to take the side of consumers wherever they may need it. Since the new health law is the biggest change in the American health care system in more than a generation, they created the Health Law Helper to give consumers accurate and unbiased information about the law and how it affects them.

Please pass it along to anyone who needs advice from a trusted organization with the consumer's best interest at heart.

Health Exchange Marketing - Finding SuperMan or (Woman)?

October 1st, 2013 marks the official kick-off of the open enrollment window for eligible Americans to enroll for health insurance through state exchanges for a January 1, 2014, effective date. The hope of course is that 40 million uninsureds sign up or they will face a penalty of the greater of $95 or 1% of adjusted gross income. The odds makers are projecting somewhere between 7-8 million enrollees will hit the buy button for 2014. While federal navigators and the administration will be touting how to enroll ALL Americans, the insurance carriers who have selectively chosen their markets will take a different tactic. If history repeats itself, the last mass public-private health enrollment push dates back to the Bush-era when Medicare Advantage plans first became available to the over 65 crowd. A regulatory official once shared with me they had to take enforcement actions against an insurance company promoting their Medicare Advantage plans after learning the carrier held their informational meetings on the top floor of a strip mall with stair-only access. Ask yourself if you would rather insure a senior citizen that can walk up a flight of stairs or one that rolls onto an elevator in the latest personal electric transport chair endorsed by Burl Ives? This post is not meant to judge our for-profit businesses for pursuing legal tactics that enhance profitability for their shareholders. Profit or perish is the maxim for any business. The far greater concern is what happens when public and private insurance pools go after the best customers. History shows us that private enterprise usually wins out when it comes to marketing consumer goods and services.

The big five health carriers are poised to spend $1 billion or more to attract millions of new customers who never have payed health premiums before. Despite the appeal of a glossed-up "Kathleen Sebelius flyer" produced by the Secretary of Health and Human Services office for "Navigator" distribution, finding "Superman" will not be a fair gunfight for the public Exchanges. Let's face it ... the Madison Avenue-style advertising budgets funded by the largest insurance carriers will be playing in a different league. If you haven't noticed ... the largest health carriers are now sponsoring more marathons, cycling teams, triathlons, mob and ultra events than ever before. It's health marketing 101, the audience there is worth the brand impression.

Don't expect to see a carrier-sponsored exchange ad next time you're picking up your blood pressure meds at the local CVS. Instead, check inside a Men's Health or Seventeen magazine to find out how to enroll ... or better yet ... run a local 10k and post your results on your Facebook timeline. The chances are in this new digital economy, there is already enough "big data" that is aggregated on you to predict your health risk. You will know your health status by how aggressively you are sought after.

Is the obesity crisis hiding a bigger problem?

From Leonardo da Vinci to Dr. Atkins, society often ridicules those with different points of view. Here Dr. Peter Attia discusses some compelling reasons why we might want to question the conventional thinking around obesity and insulin resistance. Dr. Peter Attia's presentation has nearly garnered 1MM views and it's worth the watch.

As a young surgeon, Peter Attia felt contempt for a patient with diabetes. She was overweight, he thought, and thus responsible for the fact that she needed a foot amputation. But years later, Attia received an unpleasant medical surprise that led him to wonder: is our understanding of diabetes right? Could the precursors to diabetes cause obesity, and not the other way around? A look at how assumptions may be leading us to wage the wrong medical war.

Both a surgeon and a self-experimenter, Peter Attia hopes to ease the diabetes epidemic by challenging what we think we know and improving the scientific rigor in nutrition and obesity research.

Source: TEDMED - April 2013